Blog

International Health Insurance for Bangladeshis: Ultimate Expat Guide

When you pack your bags to move abroad from Bangladesh—whether you are a corporate professional relocating to the UAE, a student heading to the UK, or an expat settling in North America—the excitement is unmatched. However, amid the chaotic rush of managing visas, flights, and accommodations, many global citizens forget to secure one critical element until the last minute: cross-border healthcare access.

Adjusting to an unfamiliar medical infrastructure in a new country can get overwhelming very quickly. A sudden emergency or unexpected illness can easily wipe out your hard-earned savings if you do not have a strong financial shield in place.

This comprehensive guide breaks down the mechanics of cross-border medical coverage, answers the core question of how does international health insurance work, and explains why it is an indispensable asset for Bangladeshi global citizens.

What is International Health Insurance?

To build a reliable safety net, it helps to establish a clear definition upfront: what is international health insurance?

Unlike standard health insurance in Bangladesh, which covers you exclusively within national borders, international health insurance (often called global medical insurance) is specifically designed for expats, digital nomads, and international students living or working abroad for extended periods.

Instead of restricting your medical care to a single country, a global policy provides comprehensive, continuous medical coverage across continents. Whether you need a routine health checkup in Singapore, emergency treatment in London, or a specialist consultation in Dubai, an international plan ensures you have hassle-free access to top-tier private healthcare networks worldwide.

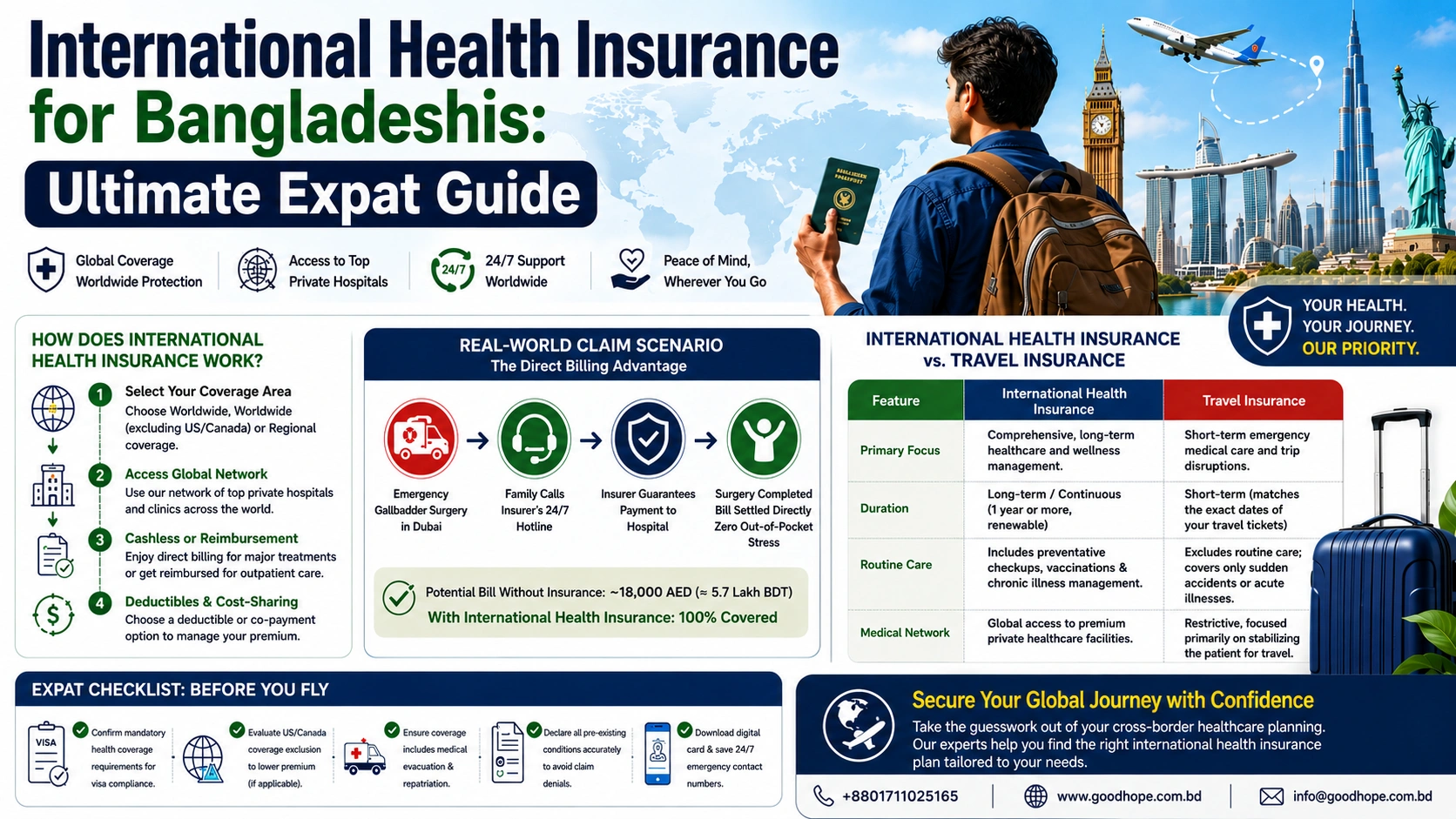

How Does International Health Insurance Work?

Understanding the operational framework of global coverage helps you maximize your benefits when you need care. If you are wondering how does international health insurance work on a day-to-day basis, the process follows a structured, cross-border system:

1. Selection of Geographical Coverage Area

When setting up your policy, you customize your geographical zone. Most international underwriters categorize plans into three main tiers:

- Worldwide (including the US & Canada): Offers unrestricted global coverage, including countries known for hyper-expensive healthcare systems.

- Worldwide (excluding the US & Canada): Provides extensive global protection at a significantly lower premium by omitting North American medical networks.

- Regional Tiers: Focuses strictly on specific geographical zones, such as Southeast Asia, Europe, or the Middle East.

2. Accessing the Global Private Medical Network

International insurance providers maintain massive, pre-vetted networks of private hospitals, clinics, and medical specialists globally. When you require medical attention, you simply choose an approved provider within that network. For major procedures or inpatient care, you typically request a "Pre-Authorization" from your insurer, allowing them to coordinate directly with the medical facility.

3. Direct Billing (Cashless) vs. Reimbursement

- Direct Settlement (Cashless): For scheduled surgeries or overnight hospital stays, the insurer settles the bills directly with the network hospital. You can walk out after treatment without paying hefty out-of-pocket fees.

- Reimbursement: For minor outpatient consultations or prescription drugs, you pay the local clinic upfront, upload a copy of your invoice and medical report to your insurer's digital portal or app, and receive the reimbursed funds in your bank account.

[Medical Need Arises Abroad] ---> [Check Insurer's App for Network Hospital] ---> [Pre-Authorize or Direct Bill] ---> [Treatment Completed with Zero Out-of-Pocket Stress]

4. Deductibles and Cost-Sharing Mechanisms

To keep your monthly or annual premiums affordable, you can opt for a deductible (the fixed amount you agree to pay out of pocket before the insurance coverage kicks in) or a co-payment (a fixed percentage of each medical bill you share with the insurer).

Real-World Claim Scenario: The Direct Billing Advantage

Our experience working with international clients highlights exactly why proper global coverage is vital. Consider the case of a Bangladeshi software engineer who recently relocated to Dubai. Two months into his stay, he required emergency gallbladder surgery.

Without international coverage, he would have faced an immediate out-of-pocket hospital bill of roughly 18,000 AED (approximately 5.7 Lakh BDT) before being admitted to a premium private clinic.

Because he possessed a valid global policy with Worldwide coverage, his family contacted the insurer's 24/7 hotline from the emergency room. The insurer issued an immediate guarantee of payment to the hospital. The surgery was completed successfully, and the entire bill was settled directly between the insurer and the hospital—allowing the engineer to focus entirely on recovery rather than financial stress.

International Health Insurance vs. Travel Insurance

Many Bangladeshi expats make the high-risk mistake of relying entirely on standard travel insurance for long-term stays abroad. While both offer cross-border medical protection, their scope, purpose, and durations are completely different.

Comparison Matrix: Global Health vs. Travel Insurance

| Feature | International Health Insurance | Travel Insurance |

|---|---|---|

| Primary Focus | Comprehensive, long-term healthcare and wellness management. | Short-term emergency medical care and trip disruptions. |

| Duration | Long-term or continuous (usually 1 year or more, renewable annually). | Short-term (typically matches the exact dates of your travel tickets). |

| Routine Care | Includes preventative checkups, vaccinations, and chronic illness management. | Excludes routine care; covers only sudden accidents or acute illnesses. |

| Medical Network | Global access to premium private healthcare facilities. | Restrictive, focused primarily on stabilizing the patient for travel. |

If you are taking a short 2-week vacation or business trip, a standard travel insurance in Bangladesh policy is perfectly adequate. However, if you are relocating for work, business, or study, international health insurance is a non-negotiable requirement.

Why Standard Bangladeshi Health Policies Fall Short Abroad

Local health insurance policies in Bangladesh are optimized for the domestic healthcare market. They calculate premiums based on localized treatment costs at hospitals in cities like Dhaka, Chittagong, or Sylhet.

If you attempt to use a domestic policy to cover a medical procedure in a country like Singapore, Thailand, or Germany, you will run into several severe barriers:

- Territorial Restrictions: Standard local policies instantly void their coverage the moment you cross international borders.

- Currency and Inflation Gaps: Local limits (e.g., a cap of 5 Lakh BDT) are completely inadequate when facing international private medical bills, which can easily scale into tens of thousands of dollars or euros.

- Lack of Cashless Infrastructure: Local insurers rarely maintain direct billing relationships with major international healthcare networks, forcing you to pay astronomical costs up front.

Key Factors for Bangladeshis to Consider Before Buying

In our experience, when evaluating an international health insurance provider, you should look closely at these three critical parameters to ensure your policy delivers real-world value:

1. Pre-Existing Medical Conditions

If you have an ongoing health issue (such as diabetes, hypertension, or cardiovascular conditions), you must declare it during the application process. Some global underwriters will exclude these conditions entirely, while others will cover them after a specific waiting period or in exchange for a premium loading fee.

2. Underwriting Flexibility (FMU vs. Moratorium)

- Full Medical Underwriting (FMU): You provide your complete medical history up front. This offers absolute clarity on what is covered and what is excluded before you ever file a claim.

- Moratorium Underwriting: The insurer automatically excludes any conditions you have had in the past 2–5 years without requiring a lengthy medical form up front. If you remain symptom-free for a set period, those conditions may eventually be covered.

3. Regulatory and Visa Compliance

Many destinations enforce strict healthcare insurance mandates for incoming expats. For example, international students heading to the UK must pay the Immigration Health Surcharge (IHS), but often supplement it with private international coverage to access faster private networks. Similarly, countries in the Schengen Zone or the UAE have specific minimum coverage limits required for visa approval.

Expat Checklist: Securing Your Global Health Strategy

Before you catch your flight from Hazrat Shahjalal International Airport, ensure you have checked off these essential healthcare steps:

- Confirmed whether your destination country requires mandatory health coverage for visa compliance.

- Evaluated whether the US/Canada coverage exclusion applies to your travel routes to lower your premium.

- Checked if your global policy includes emergency medical evacuation and repatriation back to Dhaka.

- Declared all pre-existing medical conditions accurately to avoid unexpected claim denials.

- Downloaded your digital insurance card and stored the insurer's emergency 24/7 contact numbers on your phone.

Secure Your Global Journey with Confidence

Relocating across borders is a life-changing adventure. Protecting your health and financial well-being should never be left to chance or handled with guesswork. By choosing a robust, globally recognized international health policy, you ensure that no matter where your career, education, or lifestyle takes you, premium medical care is always within reach.

At Goodhope, we specialize in simplifying complex insurance decisions for individuals and corporate entities alike. If you need help analyzing global policies, understanding geographical coverage options, or finding the perfect balance between premium costs and comprehensive benefits, we are here to guide you.

Take the guesswork out of your cross-border healthcare planning. Contact us today to speak with our dedicated consultants and secure a tailored, high-value insurance strategy for your international journey.

Frequently Asked Questions (FAQ)

Q1: Can I use my local Bangladeshi health insurance card abroad?

No, you cannot. Local policies are built strictly for the domestic market and settle bills in BDT. They lack the international networks and regulatory approvals required to cover your treatments outside Bangladesh.

Q2: Does international health insurance cover pre-existing conditions?

It depends on the provider. Some global insurers will cover pre-existing illnesses (like diabetes) after a specific waiting period, usually 12 to 24 months. Others may include them immediately for a higher premium, or exclude them completely.

Q3: Is global medical insurance mandatory for student or work visas?

Yes, many countries require it by law. For example, countries in the Schengen Zone and the UAE enforce strict minimum health insurance limits that you must meet before they approve your visa application.

Q4: What happens if I visit a hospital outside my insurer's network?

You pay the medical bills out of pocket first. Ensure you save all original prescriptions and invoices. You can then upload these documents to your insurer’s digital portal to receive a reimbursement directly into your bank account.

Q5: How can I lower my premium without cutting essential coverage?

You can select a higher deductible, meaning you agree to pay a small fixed amount out of pocket before the insurance kicks in. Additionally, excluding US/Canada coverage from your policy zone instantly drops your premium by 30% to 50%.