Blog

How Does Life Insurance Work? A Simple Guide for BD Families

Thinking about the future can be overwhelming, especially when it comes to financial security. For families in Bangladesh, ensuring that loved ones are protected against life’s uncertainties is a top priority. Whether you are a parent looking out for your children’s higher education, a business owner safeguarding family assets, or an executive planning a peaceful retirement, understanding life insurance is the first step toward long-term peace of mind.

Life insurance is not a luxury; it is a foundational pillar of smart financial planning. This comprehensive, expert-backed guide breaks down everything you need to know about how life insurance works in Bangladesh, the exact products available in our local market, and how to choose the right financial safety net for your family.

1. What is Life Insurance and How Does it Work?

At its core, Life Insurance is a legally binding contract between you (the policyholder) and an insurance company. In exchange for regular payments (called premiums), the insurance provider promises to pay a designated financial sum (the Sum Assured) to your chosen family members (nominees or beneficiaries) if you pass away during the policy term, or to you directly if you survive the policy's maturity date.

In Bangladesh, the entire life insurance ecosystem is strictly regulated and supervised by the Insurance Development and Regulatory Authority (IDRA) under the Insurance Act 2010. This state regulation ensures transparency, financial solvency among providers, and the ironclad protection of policyholder rights.

Key Terms You Must Know:

- Proposer / Policyholder: The person who buys the insurance policy and pays the premium.

- Life Assured: The individual whose life is covered by the policy (usually the primary breadwinner).

- Sum Assured: The guaranteed base amount that the insurance company promises to pay out.

- Premium: The fixed money you pay monthly, quarterly, half-yearly, or annually to keep the policy active.

- Nominee: The family member(s) you select to receive the insurance payout in your absence.

- Maturity Benefit: The amount paid to you if you successfully outlive the duration of your insurance policy.

- Bonus / Profit: Additional financial returns declared annually by companies on "with-profits" policies, driven by the insurer's investment yields.

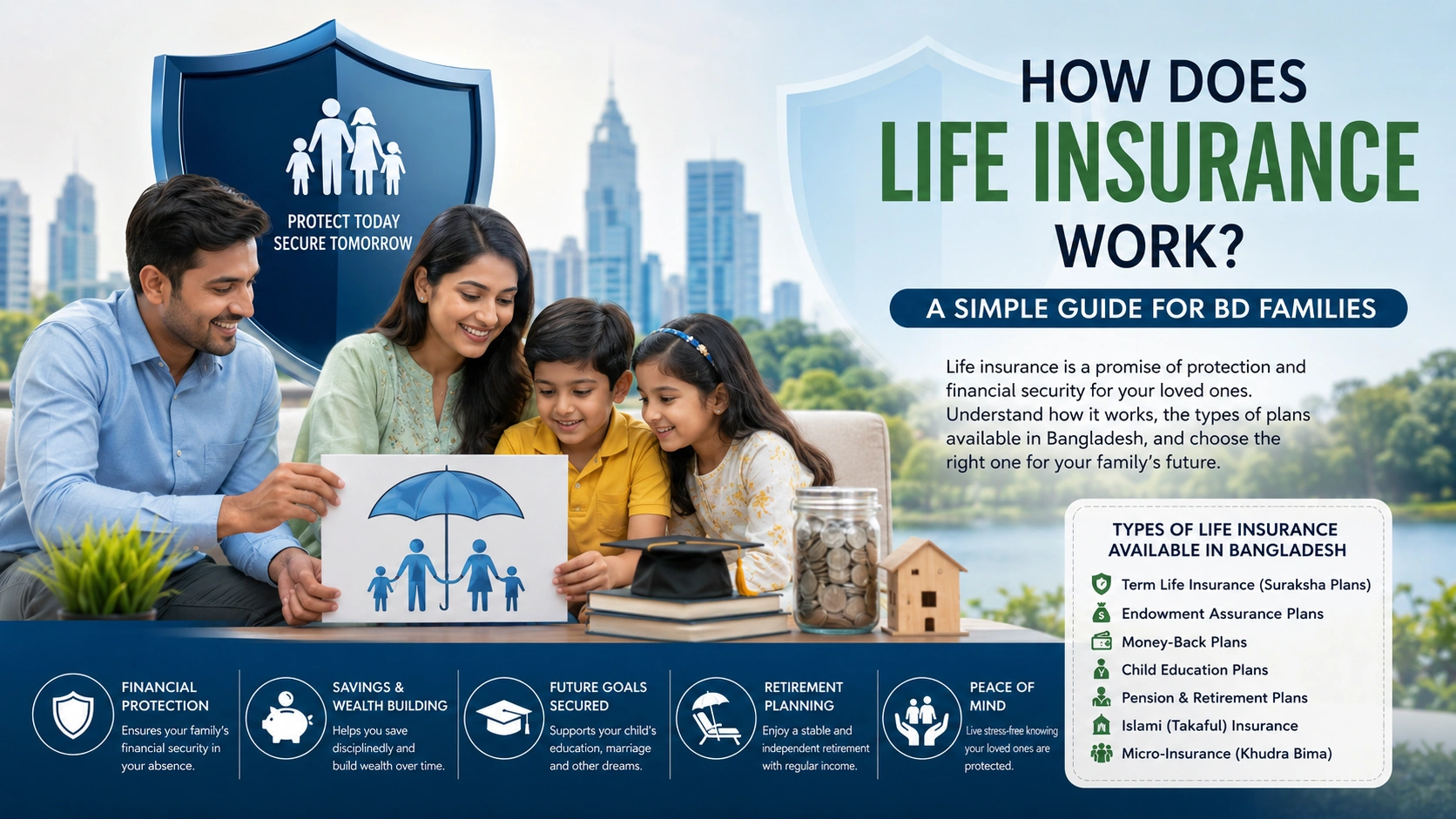

2. Types of Life Insurance Products Available in Bangladesh

The Bangladeshi insurance market offers a wide variety of life insurance products tailored to different socio-economic needs, savings horizons, and religious values. Locally, these plans are broadly categorized under Ordinary Life (Ekok Bima) and Micro-Insurance (Khudra Bima).

Below is an exhaustive breakdown of all major life insurance plans currently operational under IDRA guidelines:

A. Term Life Insurance (Suraksha Plans)

Term insurance is pure, absolute financial protection. It features no savings element , meaning it does not pay any money back if you survive the term. Because the insurance company only pays out in the event of death, the premiums are incredibly low.

- Best For: Individuals seeking maximum financial coverage for their family at the lowest possible cost, or protecting liabilities like a home loan.

- Local Market Example: MetLife Bangladesh's Mera Term or specialized term structures from corporate providers.

B. Endowment Assurance Plans (With or Without Profits)

This is the most traditional and highly popular life insurance structure in Bangladesh. It effectively blends savings and protection.

- How it Works: You choose a term (e.g., 10, 15, or 20 years). If something happens to you during this period, your nominee gets the full Sum Assured plus accrued bonuses. If you outlive the term, you receive the full Sum Assured and the accumulated bonuses as a lump sum maturity benefit.

- Best For: Long-term disciplined savings paired with basic life cover.

C. Multi-Stage / Anticipated Endowment (Money-Back Plans)

Recognizing that families often need liquid cash before a 20-year policy matures, local insurers developed installment-based payment plans (commonly referred to as Three-Payment, Four-Payment, or Biennial plans).

- How it Works: The insurer pays out a specified percentage of the Sum Assured at regular intervals (e.g., every 3, 4, or 5 years) during the active policy term. The remaining balance, along with all accumulated bonuses, is paid out at maturity. Crucially, if death occurs at any point, the full Sum Assured is paid to the nominee, regardless of how many survival installments were already drawn.

- Best For: Funding predictable milestone expenses like a child's secondary school admission or intermediate weddings.

D. Child Education & Protection Assurance Plans

These policies are specifically engineered to guarantee that a child’s educational milestones are funded, even if the primary earning parent passes away.

- The Waiver of Premium Feature: If the payor (parent) passes away prematurely, the insurance company immediately waives all future premium payments. The policy stays completely active, and the child receives regular educational stipends or a massive lump sum at the scheduled maturity date.

- Best For: Parents wanting to shield their children's educational path from sudden loss of household income.

E. Pension & Retirement Assurance Plans

Designed to offer financial independence during your post-work years, these plans transition your active savings into a reliable income stream.

- How it Works: You pay premiums during your working life. Upon reaching a designated retirement age (e.g., 55, 60, or 65), the policy converts into a pension, paying you regular monthly, quarterly, or annual payouts along with medical benefit extensions.

- Guaranteed Period: Most local plans offer a guaranteed payout period (often 10 years). If you pass away early into your retirement, your nominee continues to receive the pension for the remainder of that guaranteed window.

F. Islami Insurance / Takaful

For families seeking Shariah-compliant financial protection, Takaful functions on the Islamic principles of mutual cooperation (Ta'awun) and donation (Tabarru).

- How it Works: Policyholder premiums are pooled into a collective fund managed under Mudarabah or Wakala structures. The funds are invested strictly in Halal avenues (like Islamic Sukuk or Islamic banks), completely avoiding interest (Riba).

- Local Market Example: Providers like Akij Takaful Life Insurance, Prime Islami Life, or the dedicated Takaful wings of traditional insurers.

G. Specialized Cultural & Milestone Plans (Hajj & Mohorana)

Unique to the cultural tapestry of Bangladesh, IDRA-approved insurers provide hyper-targeted endowment plans:

- Hajj Bima Plan: Structured savings over a selected timeline specifically calculated to cover the logistical expenses of performing the Holy Hajj, bundled with life cover during the journey.

- Mohorana Bima Plan: Designed to assist Muslim grooms in systematically saving towards and fulfilling their mandatory financial obligation of Dower (Mohorana) to their spouses at or post-marriage.

H. Deposit Pension Scheme (DPS) & Micro-Insurance

Aimed predominantly at low-income groups and the massive rural population of Bangladesh.

- How it Works: Micro-DPS products allow monthly premium deposits starting as low as TDT 200 to TDT 1,000. It fosters institutional financial inclusion across villages, protecting small businesses and day-laborer households from descending into debt due to medical emergencies or sudden family deaths.

3. Comparing Life Insurance Products at a Glance

| Policy Type | Primary Objective | Death Benefit | Maturity Benefit | Ideal Audience |

|---|---|---|---|---|

| Term Life | Pure, low-cost protection | Full Sum Assured paid to nominee | None (No cash back) | Young breadwinners with tight budgets or high loans. |

| Endowment | Forced savings + Protection | Full Sum Assured + Bonuses | Full Sum Assured + Accumulated Bonuses | Individuals planning long-term goals (e.g., buying a flat). |

| Money-Back | Liquidity + Protection | Full Sum Assured (No deductions) | Remaining Sum Assured + All Bonuses | Families needing cash injections every few years. |

| Child Protection | Securing child's future | Future premiums waived + Payouts | Stipends / Final payout made to child | Parents with young school-going children. |

| Pension Plan | Post-retirement income | Payout to nominee if premature | Regular annuity / Pension payments | Professionals looking for long-term financial security. |

| Takaful | Shariah-Compliant cover | Mutual fund payout to nominee | Share of surplus fund + Investment growth | Individuals seeking interest-free ethical investments. |

4. Crucial Information: Claims, Riders, and Tax Benefits

Navigating life insurance effectively requires looking past the core policy types to understand the operational advantages and procedures built into the system.

Optional Add-On Coverages (Riders)

You can significantly boost a basic life policy by attaching supplementary contracts known as riders for a nominal cost:

- Critical Illness (CI) Rider: Automatically pays out a substantial percentage of your sum assured immediately upon the medical diagnosis of severe conditions (like cancer, heart attack, or stroke), giving you vital liquid capital for treatment.

- Accidental Death Insurance (ADI): Doubles the payout to your nominee if your passing is caused directly by an accident.

- Permanent Total Disability (PTD): Waives premiums and provides regular payouts if an accident causes a permanent loss of limbs or eyesight, stopping you from working.

The Power of Fiscal Incentive: Tax Rebate Benefits

One of the most immediate benefits of buying life insurance in Bangladesh is the legitimate Tax Rebate. Under the National Board of Revenue (NBR) rules, the premium you pay toward a life insurance policy (up to a specific legal percentage of the total income or sum assured) qualifies for a direct deduction from your annual income tax liability. Additionally, the final maturity amount received from a life insurance company is entirely tax-free.

How to Claim Life Insurance Payouts

The ultimate benchmark of an insurance company is its Claims Payout Ratio. When a claim arises, following a precise sequence prevents unnecessary delays.

1. Immediate Notification: Within 30–90 days.

The nominee or legal heir must formally inform the insurance company of the policyholder's demise via a written claim notice or through the provider's digital portal.

2. Document Gathering: Crucial Checklist.

Collect all mandatory verified paperwork: Original Policy Document, Attested Death Certificate (from Ward Councilor or Union Parishad), Medical Reports, Nominee's NBR-compliant NID, and bank details.

3. Company Verification: Underwriting Review.

The insurer verifies the authenticity of the documents. For natural deaths, this is fast; accidental or early-policy deaths (within 2 years of buying) may undergo a brief standard validation.

4. Fund Settlement: Direct Bank Transfer.

Upon approval, the insurer executes a direct electronic fund transfer (BEFTN) or issues a formal bank cheque to the nominee for the total eligible sum.

5. Frequently Asked Questions (FAQ)

Q: Can I take out multiple life insurance policies from different companies?

A: Yes. You can hold multiple policies across different insurers (e.g., holding a Term plan with MetLife and a Child Education scheme with Guardian Life). However, you must transparently disclose your existing insurance coverages during the application underwriting phase.

Q: What happens if I stop paying my premiums after a few years?

A: If you stop paying premiums during the initial years (typically less than 2 consecutive years), your policy will lapse, and you lose coverage. However, if you have paid premiums for 2 or 3 complete years, the policy acquires a Surrender Value or converts into a "Paid-Up Policy" with a reduced sum assured, ensuring your money isn’t totally lost.

Q: Is medical check-up mandatory before buying life insurance?

A: Not always. For younger age groups and lower Sum Assured amounts, companies offer Non-Medical limits. However, if you are above a certain age (typically 45+) or applying for a massive Sum Assured, standard medical examinations (blood tests, ECG) are mandatory and usually funded by the insurer.

Q: How does Bankassurance work in Bangladesh?

A: Following recent IDRA and Bangladesh Bank clearances, Bancassurance allows commercial banks in Bangladesh to act as corporate agents for insurance companies. You can now conveniently review, purchase, and pay premiums for life insurance products directly through your bank account or local branch.

Conclusion: Securing Your Corner of the World

Life insurance is ultimately an act of love and responsibility. It ensures that the dreams you hold for your family—whether it's home ownership, elite education, or a peaceful lifestyle—remain fully protected, no matter what curveballs life throws your way.

At GoodHope, we are dedicated to transforming how risk management works across Bangladesh. We blend modern digital convenience with absolute transparency, making it easy to protect your family's financial roadmap. From protecting your health with dependable health insurance in Bangladesh to optimizing your business operations, our mission is to deliver elite, hassle-free security to your ecosystem.

Take control of your family's tomorrow. Explore our comprehensive, family-focused digital insurance solutions today.